Six months ago, if you were building something with AI, you probably defaulted to an American API. Claude for coding, GPT for chat, Gemini if you were on a budget. That default has quietly been rewritten. As of May 2026, Chinese open-weight models now handle over 60% of all tokens flowing through OpenRouter, the world's largest model aggregation platform. And the thing is — most developers I talk to still think this is a future problem.

How 60% Happened

The numbers are worth sitting with for a second. In February 2026, Chinese models surpassed US models on OpenRouter for the first time. By April, the gap was decisive. Xiaomi's MiMo-V2-Pro alone commanded 21.1% of weekly token volume, three times the share of OpenAI's GPT-5.5. During the week of April 27 to May 3, Chinese model usage surged 81.7% week-over-week while US model usage dropped 34.6%.

The top six providers by weekly token volume on OpenRouter's latest rankings are all Chinese: Xiaomi (MiMo-V2-Pro, 4.21T), Alibaba (Qwen 3.6 Plus, 2.77T), MiniMax (M2.7, 1.62T), Zhipu AI (GLM-5, 1.12T), DeepSeek (V3.2, 1.11T), and StepFun (Step 3.5 Flash, 1.07T). OpenAI sits seventh at ~1.5T.

A year ago Chinese models held less than 2% of this platform.

| Provider | Flagship Model | Weekly Tokens | Share |

|---|---|---|---|

| Xiaomi | MiMo-V2-Pro | 4.21T | 21.1% |

| Alibaba | Qwen 3.6 Plus | 2.77T | 13.9% |

| MiniMax | MiniMax M2.7 | 1.62T | 8.1% |

| Zhipu AI | GLM-5 | 1.12T | 5.6% |

| DeepSeek | DeepSeek V3.2 | 1.11T | 5.6% |

| StepFun | Step 3.5 Flash | 1.07T | 5.3% |

| OpenAI | GPT-5.5 | ~1.5T | 7.5% |

The Price Gap Nobody Can Ignore

Here is the real story. Chinese models cost between one-tenth and one-twentieth of comparable US APIs. The numbers are not subtle.

A daily research agent processing 5 million tokens costs $125 per day when routed through Claude. The same workload costs $0.70 on DeepSeek V3.2. Running a standard benchmark eval suite: $4,811 with Claude, $544 with Zhipu's GLM. MiniMax M2.5 charges $0.30 per million input tokens. Claude Opus 4.6 charges $5.00.

That is a 17x difference for performance that, on most practical tasks, is functionally indistinguishable.

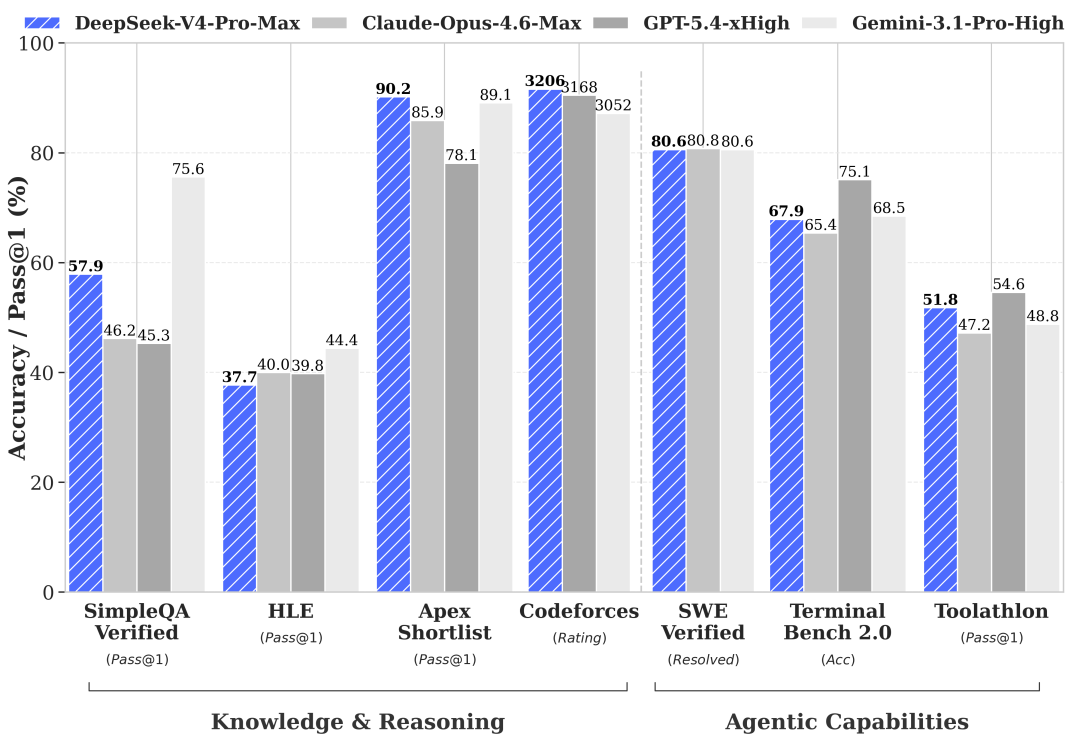

MiniMax M2.5 scored 80.2% on SWE-Bench Verified against Claude Opus 4.6 at 80.8%. Kimi K2.6 became the first open-weight model ever to beat GPT-5.4 on SWE-Bench Pro, posting a 58.6 score against GPT-5.4's 57.7. DeepSeek V4 Pro (Max) scores 87 on the BenchLM Intelligence Index against GPT-5.4 at 88. These are not budget-tier numbers. These are frontier numbers at garage-sale prices.

Architecture: The Forced Innovation Story

The US chip export restrictions that aimed to slow down Chinese AI development had an unexpected side effect. Chinese labs could not easily access NVIDIA's latest hardware for training. Huawei's Ascend 910B chips, the domestic alternative, failed during DeepSeek V4 training runs, forcing an architecture pivot back to NVIDIA. But the constraint also drove intense efficiency innovation.

Every top Chinese model uses Mixture-of-Experts architecture. DeepSeek V4 is estimated at 1 trillion total parameters with ~37B active per token. Kimi K2.6 is also 1T MoE. Step 3.5 Flash packs a 196B MoE with an AIME 2025 math score of 97.3, outperforming models many times its size. Qwen 3.6 Plus offers a 1-million-token context window. GLM-5.1 beats Claude Opus 4.6 on a key coding benchmark.

The thread running through all of them: they achieve comparable benchmarks with far less compute per token, and they pass those savings straight to the developer.

Where They Still Trail

This is not a story of total victory. Chinese models have real weaknesses.

Multimodal capability lags by roughly a generation. Dense video reasoning is notably weaker than Gemini or GPT. English-language creative writing sometimes carries an ESL tone. The models are trained on predominantly Chinese data and the English output can feel slightly off in narrative contexts. Tool-call JSON occasionally arrives with format issues that require robust wrapper validation. And the agent ecosystem around these models (MCP server support, IDE integrations, deployment tooling) is still catching up to the Anthropic and OpenAI ecosystems.

But here is the thing. Developers are choosing these models anyway. The quality delta does not justify the price delta. That is a structural shift, not a temporary one.

What the Shift Actually Means

The OpenRouter data only captures one slice of the market: developer-led API usage, startup workloads, research experiments, automation pipelines. It does not capture the enterprise contracts (the Fortune 500 deal with OpenAI, the government procurement with Anthropic). It does not capture the integrated services like GitHub Copilot or Microsoft 365.

But that slice matters. It is the slice where the next generation of AI products gets built. When 80% of young AI companies using open-source stacks now incorporate Chinese models, according to OpenRouter's data, you are watching the startup ecosystem vote with its wallet.

The deeper trend is this. For the last two years, the AI industry has been organized around the assumption that a small number of US labs would maintain an insurmountable quality lead. That assumption is not holding. The gap has compressed to roughly 3-6 months on benchmarks, and the price gap is measured in orders of magnitude.

Google can afford to lose the benchmark war because it has distribution. Anthropic can win on safety and enterprise trust. But the mass of undifferentiated developers building the next wave of AI applications: they are going where the work gets done for the lowest cost. And that is now, emphatically, China.

What Surprised Me

I did not expect Xiaomi to be the token volume leader. Of all the Chinese labs, a phone company is the one sitting at 21% of OpenRouter traffic? That was not on my 2026 bingo card. But it makes sense when you look at the Apache 2.0 licensing and absurdly low pricing. MiMo is what happens when a hardware company decides to use AI as a loss leader for its device ecosystem.

The other thing that surprised me: how quietly this happened. There was no single breakthrough moment. No "China surpasses US" headline that went viral. It was hundreds of thousands of individual API routing decisions, each one made by a developer who looked at the Claude pricing page, looked at the DeepSeek pricing page, and switched. A death by a thousand cost optimizations.

The Chinese labs are not done. Kimi K3 is expected later this year with 1M context and 3-4T parameters. DeepSeek V4 is already live. Price compression is expected to push toward a $0.05 per million token floor. If you are paying US API prices today and your workload is not enterprise-locked, you should probably start experimenting with OpenRouter routing. The experiment will likely save you 90%. And the models are good enough that you probably will not switch back.

Sources

- OpenRouter State of AI 2025/2026 report (100T token analysis)

- Awesome Agents: "Chinese Models Claim 60% of OpenRouter Token Traffic" (May 22, 2026)

- TrendingTopics: "Chinese AI Models Overtake US Rivals in Global Token Consumption" (May 2026)

- TokenMix Research Lab: "Best Chinese AI Models 2026" (Q2 Update)

- BenchLM.ai: "Best Chinese LLMs in 2026" (May 22, 2026)

- DeepSeek API Docs: V4 Preview Release (April 24, 2026)

- Understanding AI: "The Best Chinese Open-Weight Models" (2026)

- DeepLearning.ai The Batch: "Kimi K2.6 Challenges Open-Weights Champs"

- CNBC: "Anthropic weighs raising funds at $900B valuation" (April 29, 2026)

- Forbes: "Anthropic's $900 Billion Funding Round Set To Surpass OpenAI" (May 4, 2026)

- Build Fast with AI: "AI News Today (May 25, 2026)"